scenario generation / reduction

Multistage stochastic programming for the optimal bid of a wind-thermal power production pool with battery storage.

Fri, 07/08/2022 - 11:26 — admin| Publication Type | Conference Paper |

| Year of Publication | 2022 |

| Authors | F.-Javier Heredia; Ignasi Mañé; Marlyn Dayana Cuadrado Guevara |

| Conference Name | EURO 2022 |

| Conference Date | 03-06/07/2022 |

| Conference Location | Espoo, Finland. |

| Type of Work | Invited presentation |

| ISBN Number | 978-951-95254-1-9 |

| Key Words | research; multistage stochastic programming; virtual power plants; unit commitment |

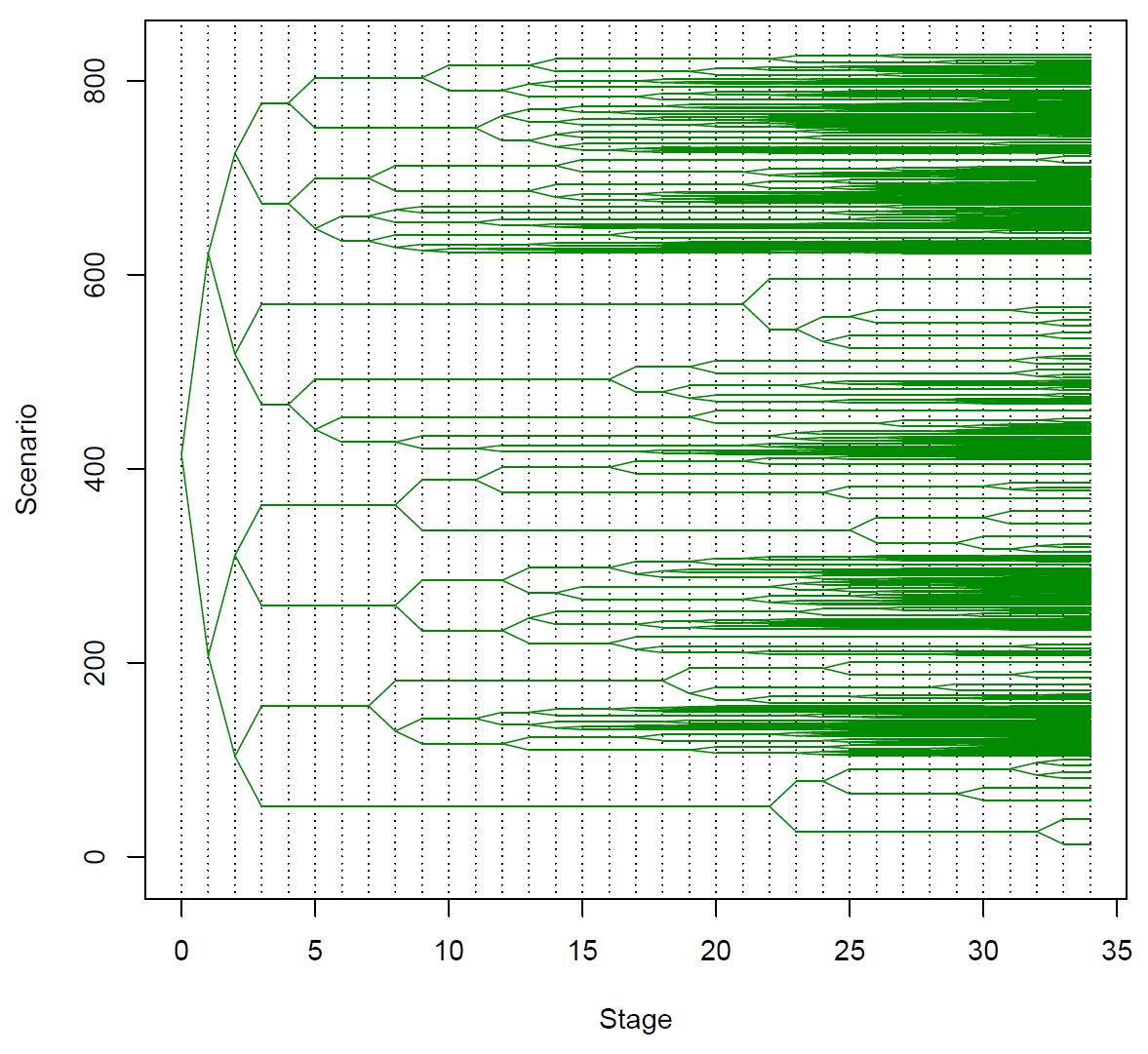

| Abstract | In this study we present a multistage stochastic programming model to find the joint optimal bid to electricity markets of a pool of dispatchable (thermal) and non-dispatchable (wind) production units with battery storage facilities. The assumption is that these programming units are operated by the same utility that, previous to the market clearing, has to dispatch some bilateral contracts with the joint production of the production pool. The multistage model mimics the multimarket bidding process in the Iberian Electricity Market (MIBEL). First, the utility has to decide how to cover the energy of the bilateral contracts with the available units. Second, the production capacity of each unit, not allocated to the bilateral contracts, must be offered to the seven consecutives spot markets (day-ahead and six intraday markets) plus the secondary reserve market (the most relevant ancillary services market). The stochasticity of the electricity clearing prices and the hourly generation of the wind-power units is considered. The stochastic process associated to this multistage decision-making process is modelled through multistage scenario trees with thirty-four stages that are built from forecasting models based on real data of the Iberian Electricity Market. The numerical results show the advantage of the joint operation of the pool of production units with an increase of the overall expected profits, mainly due to a strong reduction of the operational costs. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Multistage Scenario Trees Generation for Electricity Markets Optimization

Tue, 07/13/2021 - 10:51 — admin| Publication Type | Conference Paper |

| Year of Publication | 2021 |

| Authors | Marlyn Dayana Cuadrado Guevara; F.-Javier Heredia |

| Conference Name | 31st European Conference on Operational Research. |

| Conference Date | 11-14/07/2021 |

| Conference Location | Athens |

| Type of Work | Invited presentation |

| ISBN Number | ISBN 978-618-85079-1-3 |

| Key Words | research; multistage stochastich programming; virtual power plants; electricity markets; scenarios tree generation |

| Abstract | The presence of renewables in electricity markets optimization have generated a high level of uncertainty in the data, which has led to a need for applying stochastic optimization to model this kind of problems. In this work, we apply Multistage Stochastic Programming (MSP) using scenario trees to represent energy prices and wind power generation. We developed a methodology of two phases where, in the first phase, a procedure to predict the next day for each random parameter of the MSP models is used, and, in the second phase, a set of scenario trees are built through Forward Tree Construction Algorithm (FTCA) and a modified Dynamic Tree Generation with a Flexible Bushiness Algorithm (DTGFBA). This methodology was used to generate scenario trees for the Multistage Stochastic Wind Battery Virtual Power Plant model (MSWBVPP model), which were based on MIBEL prices and wind power generation of a real wind farm in Spain. In addition, we solved three di erent case studies corresponding to three di erent hypotheses on the virtual power plant’s participation in electricity markets. Finally, we study the relative performance of the FTCA and DTGFBA scenario trees, analysing the value of the stochastic solution through the Forecasted Value of the Stochastic Solution (FVSS) and the classical VSS for the 366 daily instances of the MSWBVPP problem spanning a complete year. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Ph D. Thesis on multistage scenario tree generation for renewable energies.

Mon, 11/30/2020 - 19:40 — admin On November 30th 2020 took place the defense of the Ph.D. Thesis entittled "Multistage Scenario Trees Generation for Renewable Energy Systems Optimization", authored by Ms. Marlyn D. Cuadrado Guevara and advised by prof. F.-Javier Heredia. In this thesis a new methodology to generate and validate probability scenario trees for multistage stochastic programming problems arising in two different energy systems with renewables are proposed. The first problem corresponds to the optimal bid to electricity markets of a virtual power plant that consists on a wind-power plant plus a battery storage energy systems. The second one is the optimal operation of a distribution grid with some photovoltaic production.

On November 30th 2020 took place the defense of the Ph.D. Thesis entittled "Multistage Scenario Trees Generation for Renewable Energy Systems Optimization", authored by Ms. Marlyn D. Cuadrado Guevara and advised by prof. F.-Javier Heredia. In this thesis a new methodology to generate and validate probability scenario trees for multistage stochastic programming problems arising in two different energy systems with renewables are proposed. The first problem corresponds to the optimal bid to electricity markets of a virtual power plant that consists on a wind-power plant plus a battery storage energy systems. The second one is the optimal operation of a distribution grid with some photovoltaic production.

Multistage Scenario Trees Generation for Renewable Energy Systems Optimization

Mon, 11/30/2020 - 19:17 — admin| Publication Type | Thesis |

| Year of Publication | 2020 |

| Authors | Marlyn Dayana Cuadrado Guevara |

| Academic Department | Dept. of Statistics and Operations Research. Prof. F.-Javier Heredia, advisor. |

| Number of Pages | 194 |

| University | Universitat Politècnica de Catalunya-BarcelonaTech |

| City | Barcelona |

| Degree | PhD Thesis |

| Key Words | research; Battery energy storage systems; Electricity markets; Ancillary services market; Wind power generation; Virtual power plants; Multistage Stochastic programming; phd thesis |

| Abstract | The presence of renewables in energy systems optimization have generated a high level of uncertainty in the data, which has led to a need for applying stochastic optimization to modelling problems with this characteristic. The method followed in this thesis is Multistage Stochastic Programming (MSP). Central to MSP is the idea of representing uncertainty (which, in this case, is modelled with a stochastic process) using scenario trees. In this thesis, we developed a methodology that starts with available historical data; generates a set of scenarios for each random variable of the MSP model; defines individual scenarios that are used to build the initial stochastic process (as a fan or an initial scenario tree); and builds the final scenario trees that are the approximation of the stochastic process. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Generació d’arbres d’escenaris per a problemes d’oferta òptima en mercats d’electricitat

Mon, 08/19/2019 - 18:04 — admin| Publication Type | Tesis de Grau i Màster // BSc and MSc Thesis |

| Year of Publication | 2019 |

| Authors | Roger Serra Castilla |

| Director | F.- Javier Heredia; Marlyn D. Cuadrado |

| Tipus de tesi | BSc Thesis |

| Titulació | Grau en Estadística |

| Centre | Facultat de matemàtiques i Estadística |

| Data defensa | 01/2019 |

| Nota // mark | 9.0 |

| Key Words | teaching; scenario generation; scenario trees; electricity markets; BSc Thesis |

| Abstract | The electricity markets (EM) is a regulated system which allows producers and consumers to sell and buy energy at a given price that is fixed through an auction mechanism. Thanks to the tasks done by this system, the safe generation, transportation and distribution of electricity needed to satisfy the demand of the national population is assured. The electricity markets is made up of several markets, that can be considered either spot markets (day-ahead and intraday markets, whose trading commodity is energy) or ancillary services markets (the commodity negotiated is energy used to assure the stability of the energy delivering). On the other hand, interacting with the EM there is a wind power plant (WPP) which is in charge of the wind power energy production. A battery energy storage system (BESS) is usually associated to the WPP. The union of the WPP and the BESS is called virtual power plant (VPP). In this context, an optimization model can be presented: the WBVPP model (WPP+BESS Virtual Power Plant). The aim of this optimization model is the maximization of the expected value of the total profit of the VPP. To calculate this value, it is necessary to quantify the amount of wind power energy that fluctuates between the VPP and the EM, as well as the clearing prices of the auctions. The main purpose of this project is to obtain scenario trees using a dynamic generation algorithm in order to satisfy the need to solve, in a reasonable period of time, complex optimization problems of optimal supply of wind power plants in electricity markets. The scenarios trees that are going to be obtained include information regarding the production of wind power energy and the clearing prices of the auctions of the different studied electricity markets. In this study a scenario tree generation algorithm is presented, together with all the theoretical background needed to understand and assure a correct implementation of it, as well as the definition of the different agents that perform in the context of electricity markets. In addition to that, some data will be applied to this algorithm in order to obtain a representation of the scenario trees and to understand the interpretation of them. |

| DOI / handle | http://hdl.handle.net/2445/128065 |

| URL | Click Here |

| Export | Tagged XML BibTex |

A Multistage Stochastic Programming Model for the Optimal Bid of Wind-BESS Virtual Power Plants to Electricity Markets

Sat, 12/16/2017 - 00:00 — admin| Publication Type | Conference Paper |

| Year of Publication | 2017 |

| Authors | F.-Javier Heredia; Marlyn D. Cuadrado; J.-Anton Sánchez |

| Conference Name | 4th International Conference on Optimization Methods and Software 2017 |

| Conference Date | 16-21/12/2017 |

| Conference Location | La Havana |

| Type of Work | Invited presentation |

| Key Words | multistage; VSS; wind-BESS VPP; wind power; energy storage; battery; research |

| Abstract | One of the objectives of the FOWGEN project (https://fowgem.upc.edu) was to study the economic feasibility and optimal operation of a wind-BESS Virtual Power Plant (VPP): In [1] an ex-post economic analysis shows the economic viability of a wind-BESS VPP thanks to the optimal operation in day-ahead and ancillary electricity markets; In [2] a new multi-stage stochastic programming model (WBVPP)for the optimal bid of a wind producer both in spot and ancillary services electricity markets is developed. The work presented here extends the study in [2] with a new methodology to treat the uncertainty, based in forecasting models, and the study of the quality of the stochastic solution. [1] F-Javier Heredia et al. Economic analysis of battery electric storage systems operating in electricity markets 12th International Conference on the European Energy Market (EEM15), 2015 DOI: 10.1109/EEM.2015.7216739. [2] F-Javier Heredia et al. On optimal participation in the electricity markets of wind power plants with battery energy storage system. Submitted, under second revision. 2017. |

| URL | Click Here |

| Export | Tagged XML BibTex |

A stochastic programming model for the tertiary control of microgrids

Thu, 09/03/2015 - 10:25 — admin| Publication Type | Proceedings Article |

| Year of Publication | 2015 |

| Authors | Leire Citores; Cristina Corchero; F.-Javier Heredia |

| Conference Name | 12th International Conference on the European Energy Market (EEM15) |

| Pagination | 1-6 |

| Conference Start Date | 19-22/05/2015 |

| Publisher | IEEE |

| Conference Location | Lisbon, Portugal. |

| ISBN Number | 978-1-4673-6691-5 |

| Key Words | Microgrids; Optimization; Production; Stochastic processes; Uncertainty; Wind power generation; Wind speed; energy system optimization; microgrid; scenario generation; stochastic programming; paper; research |

| Abstract | In this work a scenario-based two-stage stochastic programming model is proposed to solve a microgrid's tertiary control optimization problem taking into account some renewable energy resource's uncertainty as well as uncertain energy deviation prices in the electricity market. Scenario generation methods for wind speed realizations are also studied. Results show that the introduction of stochastic programming represents a significant improvement over a deterministic model. |

| URL | Click Here |

| DOI | 10.1109/EEM.2015.7216761 |

| Export | Tagged XML BibTex |

A stochastic programming model for the tertiary control of microgrids

Wed, 06/24/2015 - 13:19 — admin| Publication Type | Conference Paper |

| Year of Publication | 2015 |

| Authors | Leire Citores; Cristina Corchero; F.-Javier Heredia |

| Conference Name | 12th International Conference on the European Energy Market |

| Conference Date | 19-22/05/2015 |

| Conference Location | Lisbon, Portugal |

| Type of Work | contributed presentation |

| Key Words | research; MTM2013-48462-C2-1; microgrid; stochastic programming; scenario generation; wind power |

| Abstract | In this work a scenario-based two-stage stochastic programming model is proposed to solve a microgrid’s tertiary control optimization problem taking into account some renewable energy resource’s uncertainty as well as uncertain energy deviation prices in the electricity market. Scenario generation methods for wind speed realizations are also studied. Results show that the introduction of stochastic programming represents a significant improvement over a deterministic model. |

| URL | Click Here |

| Export | Tagged XML BibTex |

A stochastic programming model for the tertiary control of microgrids

Thu, 11/27/2014 - 16:48 — admin| Publication Type | Tesis de Grau i Màster // BSc and MSc Thesis |

| Year of Publication | 2014 |

| Authors | Leire Citores |

| Director | F.-Javier Heredia, Cristina Corchero |

| Tipus de tesi | MSc Thesis |

| Titulació | Master in Statistics and Operations research |

| Centre | Faculty of Mathematics and Statistics |

| Data defensa | 27/06/2014 |

| Nota // mark | 10 MH (A with Honours) |

| Key Words | research; teaching; microgrids, stochastic programming; scenario generation; wind generation; day-ahead electricity market; imbalances; MSc Thesis |

| Abstract | In this thesis a scenario-based two-stage stochastic programming model is proposed to solve a microgrid's tertiary control optimization problem taking into account some renewable energy resource s uncertainty as well uncertain energy deviation prices in the electricity market. Scenario generation methods for wind speed realizations are also studied. Results show that the introduction of stochastic programming represents an improvement over a deterministic model. |

| DOI / handle | http://hdl.handle.net/2099.1/23235 |

| URL | Click Here |

| Export | Tagged XML BibTex |

Improving Electricity Market Price Forecasting with Factor Models for the Optimal Generation Bid

Fri, 09/06/2013 - 14:58 — admin| Publication Type | Journal Article |

| Year of Publication | 2013 |

| Authors | M.Pilar Muñoz; Cristina Corchero; F.-Javier Heredia |

| Journal Title | International Statistical Review |

| Volume | 81 |

| Issue | 2 |

| Pages | 18 (289-306) |

| Start Page | 289 |

| Journal Date | August 2013 |

| Publisher | Wiley |

| ISSN Number | 1751-5823 |

| Key Words | research; paper; electricity market prices; short-term forecasting; stochastic programming; factor models; price scenarios; Q2 |

| Abstract | In liberalized electricity markets, the electricity generation companies usually manage their production by developing hourly bids that are sent to the day-ahead market. As the prices at which the energy will be purchased are unknown until the end of the bidding process, forecasting of spot prices has become an essential element in electricity management strategies. In this article, we apply forecasting factor models to the market framework in Spain and Portugal and study their performance. Although their goodness of fit is similar to that of autoregressive integrated moving average models, they are easier to implement. The second part of the paper uses the spot-price forecasting model to generate inputs for a stochastic programming model, which is then used to determine the company's optimal generation bid. The resulting optimal bidding curves are presented and analyzed in the context of the Iberian day-ahead electricity market. |

| URL | Click Here |

| DOI | 10.1111/insr.12014 |

| Preprint | http://hdl.handle.net/2117/3047 |

| Export | Tagged XML BibTex |