unit commitment

Optimization through quantum computing

Tue, 07/25/2023 - 19:05 — admin| Publication Type | Tesis de Grau i Màster // BSc and MSc Thesis |

| Year of Publication | 2023 |

| Authors | Andrea Iglesias Munilla |

| Director | F.-Javier heredia |

| Tipus de tesi | MSc Thesis |

| Titulació | Master in Data Science |

| Centre | Facultat d'Informàtica de Barcelona |

| Data defensa | 30/06/2023 |

| Nota // mark | 9.5 |

| Key Words | teaching; unit commitment; quantum computing; QUBO |

| Abstract | This thesis explores the application of quantum computing techniques to solve Quadratic Unconstrained Binary Optimization problems, with a focus on the Unit Commitment problem. The thesis provides an introduction to quantum computing, including its mathematical foundation and the distinction between classical and quantum systems. It then discusses Variational Quantum Algorithms and explores various quantum computing platforms. Then a novel formulation of the Unit Commitment problem is presented, along with its implementation using the Qiskit library. The results obtained from the implementation are summarized, highlighting the process of using quantum computing for solving optimization problems. |

| DOI / handle | http://hdl.handle.net/2117/394532 |

| URL | Click Here |

| Export | Tagged XML BibTex |

Presentation at the EURO 2022 conference in Finland.

Fri, 07/08/2022 - 12:10 — admin

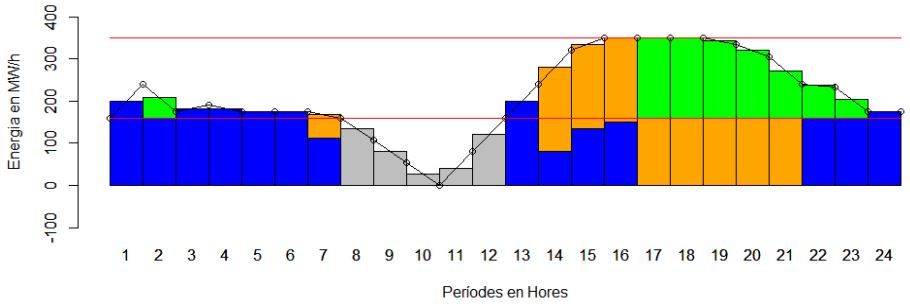

Last July 4 2022 I was invited at the EURO 2022 conference , Aalto University, Espoo, near Helsinki, to present the work Multistage stochastic programming for the optimal bid of a wind-thermal power production pool with battery storage, which is a continuation of the MSc and PhD thesis of Mr. Ignasi Manyé and Ms. Marlyn D. Cuadrado respectively. This work tackles with an extensive study along a complete timespan of on year analyzing the benefits of a joint operation of a wind and thermal generation system in the elecrticity markets and bilateral contracts. Numerical results show that the total profit increases by 13% in average, but that it can be as high as 77%, with a reduction of the thermal operation costs of 61%.

Multistage stochastic programming for the optimal bid of a wind-thermal power production pool with battery storage.

Fri, 07/08/2022 - 11:26 — admin| Publication Type | Conference Paper |

| Year of Publication | 2022 |

| Authors | F.-Javier Heredia; Ignasi Mañé; Marlyn Dayana Cuadrado Guevara |

| Conference Name | EURO 2022 |

| Conference Date | 03-06/07/2022 |

| Conference Location | Espoo, Finland. |

| Type of Work | Invited presentation |

| ISBN Number | 978-951-95254-1-9 |

| Key Words | research; multistage stochastic programming; virtual power plants; unit commitment |

| Abstract | In this study we present a multistage stochastic programming model to find the joint optimal bid to electricity markets of a pool of dispatchable (thermal) and non-dispatchable (wind) production units with battery storage facilities. The assumption is that these programming units are operated by the same utility that, previous to the market clearing, has to dispatch some bilateral contracts with the joint production of the production pool. The multistage model mimics the multimarket bidding process in the Iberian Electricity Market (MIBEL). First, the utility has to decide how to cover the energy of the bilateral contracts with the available units. Second, the production capacity of each unit, not allocated to the bilateral contracts, must be offered to the seven consecutives spot markets (day-ahead and six intraday markets) plus the secondary reserve market (the most relevant ancillary services market). The stochasticity of the electricity clearing prices and the hourly generation of the wind-power units is considered. The stochastic process associated to this multistage decision-making process is modelled through multistage scenario trees with thirty-four stages that are built from forecasting models based on real data of the Iberian Electricity Market. The numerical results show the advantage of the joint operation of the pool of production units with an increase of the overall expected profits, mainly due to a strong reduction of the operational costs. |

| URL | Click Here |

| Export | Tagged XML BibTex |

BSc Thesis on tight MILP formulation of the unit committment problem

Wed, 07/19/2017 - 11:56 — admin

L'alumne del grau de matemàtiques de l'FME Jordan Escandell ha llegit el treball fi de grau Caracterització de Formulacions Fortes del Problema Unit Commitment. Aquest projecte abordava la caracterització de formulacions fortes del problema Unit Commitment a partir de l'estudi de les diferents desigualtats proposades pels diferents autors així com la seva adaptació i possible millora en la modelització de certs problemes reals de mercats elèctrics. Els models d'optimització matemàtica obtinguts s'han implementat computacionalment i aplicat a la resolució de problemes reals d'oferta òptima a merctas elèctrics.

L'alumne del grau de matemàtiques de l'FME Jordan Escandell ha llegit el treball fi de grau Caracterització de Formulacions Fortes del Problema Unit Commitment. Aquest projecte abordava la caracterització de formulacions fortes del problema Unit Commitment a partir de l'estudi de les diferents desigualtats proposades pels diferents autors així com la seva adaptació i possible millora en la modelització de certs problemes reals de mercats elèctrics. Els models d'optimització matemàtica obtinguts s'han implementat computacionalment i aplicat a la resolució de problemes reals d'oferta òptima a merctas elèctrics.