AMPL

A model to optimize the tenant mix in a shopping centre

Mon, 06/17/2024 - 18:57 — admin| Publication Type | Conference Paper |

| Year of Publication | 2023 |

| Authors | Grace Kelly Maureira; F.-Javier Heredia |

| Conference Name | IFORS 2023 - 23rd Conference of the International Federation of Operational Research Societies |

| Conference Date | 10-14/07/2023 |

| Conference Location | Santiago, Chile |

| Type of Work | Contributed presentation |

| ISBN Number | 978-956-416-407-6 |

| Key Words | research; real state; shopping centers; tenant mix; modeling. |

| URL | Click Here |

| DOI | https://doi.org/10.1287/ifors.2023 |

| Export | Tagged XML BibTex |

Multistage stochastic programming for the optimal bid of a wind-thermal power production pool with battery storage.

Fri, 07/08/2022 - 11:26 — admin| Publication Type | Conference Paper |

| Year of Publication | 2022 |

| Authors | F.-Javier Heredia; Ignasi Mañé; Marlyn Dayana Cuadrado Guevara |

| Conference Name | EURO 2022 |

| Conference Date | 03-06/07/2022 |

| Conference Location | Espoo, Finland. |

| Type of Work | Invited presentation |

| ISBN Number | 978-951-95254-1-9 |

| Key Words | research; multistage stochastic programming; virtual power plants; unit commitment |

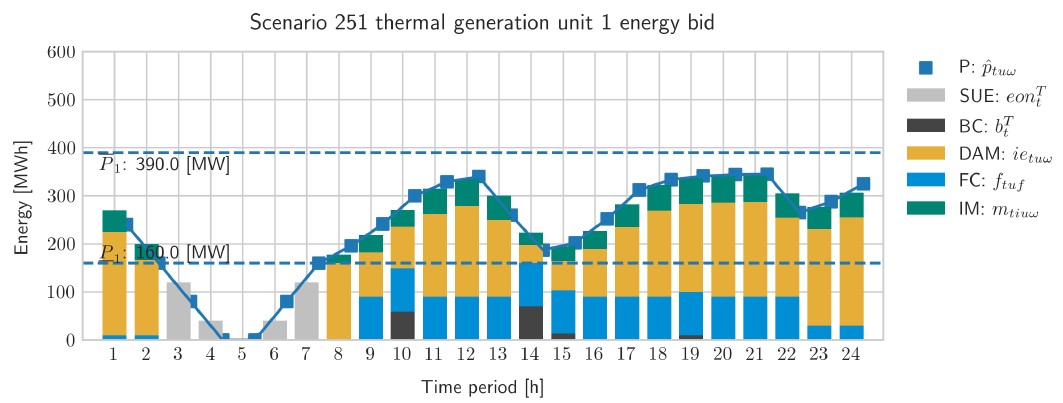

| Abstract | In this study we present a multistage stochastic programming model to find the joint optimal bid to electricity markets of a pool of dispatchable (thermal) and non-dispatchable (wind) production units with battery storage facilities. The assumption is that these programming units are operated by the same utility that, previous to the market clearing, has to dispatch some bilateral contracts with the joint production of the production pool. The multistage model mimics the multimarket bidding process in the Iberian Electricity Market (MIBEL). First, the utility has to decide how to cover the energy of the bilateral contracts with the available units. Second, the production capacity of each unit, not allocated to the bilateral contracts, must be offered to the seven consecutives spot markets (day-ahead and six intraday markets) plus the secondary reserve market (the most relevant ancillary services market). The stochasticity of the electricity clearing prices and the hourly generation of the wind-power units is considered. The stochastic process associated to this multistage decision-making process is modelled through multistage scenario trees with thirty-four stages that are built from forecasting models based on real data of the Iberian Electricity Market. The numerical results show the advantage of the joint operation of the pool of production units with an increase of the overall expected profits, mainly due to a strong reduction of the operational costs. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Multistage stochastic bid model for a wind-thermal power producer

Thu, 12/30/2021 - 13:20 — admin| Publication Type | Tesis de Grau i Màster // BSc and MSc Thesis |

| Year of Publication | 2021 |

| Authors | Ignasi Mañé Bosch |

| Director | F-Javier Heredia |

| Tipus de tesi | MSc Thesis |

| Titulació | Master in Statistics and Operations Reseafrch |

| Centre | Facultat de matemàtiques i Estadística |

| Data defensa | 18/10/2021 |

| Nota // mark | 9.5 |

| Key Words | teaching; electricity markets; multistage stochastic programming |

| Abstract | For many political and economic reasons, over the last decades, electricity markets in developed countries have been liberalised. Markets regulated by governments in which prices were set by the competent authority are now the exception. In this new setting, electricity agents, both consumers and producers, compete to maximise their pro tability in a series of auctions designed to efficiently match supply and demand. Many energy producers manage together wind and thermal generation units to meet their contractual obligations such as bilateral contracts, as well as bid on the electric market to sell their production capacity. This master thesis explore different multi-stage stochastic programming models for generation companies to nd optimal bid functions in electric spot markets. The explored models not only capture the uncertainty of electric prices of different markets and financial products, but also couples together wind and thermal generation units, offering producers that combine both technologies a more suitable approach to nd their best possible bidding strategy among the space of possible actions. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Master Thesis on electricity markets.

Wed, 12/01/2021 - 13:35 — adminOn November 2021 Mr. Ignasi Mañé presented the MsC thesis dissertation Multistage stochastic bid model for a wind-thermal power producer to opt for the master's degree in Statistics and Operations Research (UPC-UB), advised by prof. F.-Javier Heredia. This master thesis explores different multi-stage stochastic programming models for generation companies to find optimal bid functions in electric spot markets capturing the uncertainty of electric prices of different markets and financial products, and coupling together wind and thermal generation unit

Multistage Scenario Trees Generation for Electricity Markets Optimization

Tue, 07/13/2021 - 10:51 — admin| Publication Type | Conference Paper |

| Year of Publication | 2021 |

| Authors | Marlyn Dayana Cuadrado Guevara; F.-Javier Heredia |

| Conference Name | 31st European Conference on Operational Research. |

| Conference Date | 11-14/07/2021 |

| Conference Location | Athens |

| Type of Work | Invited presentation |

| ISBN Number | ISBN 978-618-85079-1-3 |

| Key Words | research; multistage stochastich programming; virtual power plants; electricity markets; scenarios tree generation |

| Abstract | The presence of renewables in electricity markets optimization have generated a high level of uncertainty in the data, which has led to a need for applying stochastic optimization to model this kind of problems. In this work, we apply Multistage Stochastic Programming (MSP) using scenario trees to represent energy prices and wind power generation. We developed a methodology of two phases where, in the first phase, a procedure to predict the next day for each random parameter of the MSP models is used, and, in the second phase, a set of scenario trees are built through Forward Tree Construction Algorithm (FTCA) and a modified Dynamic Tree Generation with a Flexible Bushiness Algorithm (DTGFBA). This methodology was used to generate scenario trees for the Multistage Stochastic Wind Battery Virtual Power Plant model (MSWBVPP model), which were based on MIBEL prices and wind power generation of a real wind farm in Spain. In addition, we solved three di erent case studies corresponding to three di erent hypotheses on the virtual power plant’s participation in electricity markets. Finally, we study the relative performance of the FTCA and DTGFBA scenario trees, analysing the value of the stochastic solution through the Forecasted Value of the Stochastic Solution (FVSS) and the classical VSS for the 366 daily instances of the MSWBVPP problem spanning a complete year. |

| URL | Click Here |

| Export | Tagged XML BibTex |

Multistage Scenario Trees Generation for Renewable Energy Systems Optimization

Mon, 11/30/2020 - 19:17 — admin| Publication Type | Thesis |

| Year of Publication | 2020 |

| Authors | Marlyn Dayana Cuadrado Guevara |

| Academic Department | Dept. of Statistics and Operations Research. Prof. F.-Javier Heredia, advisor. |

| Number of Pages | 194 |

| University | Universitat Politècnica de Catalunya-BarcelonaTech |

| City | Barcelona |

| Degree | PhD Thesis |

| Key Words | research; Battery energy storage systems; Electricity markets; Ancillary services market; Wind power generation; Virtual power plants; Multistage Stochastic programming; phd thesis |

| Abstract | The presence of renewables in energy systems optimization have generated a high level of uncertainty in the data, which has led to a need for applying stochastic optimization to modelling problems with this characteristic. The method followed in this thesis is Multistage Stochastic Programming (MSP). Central to MSP is the idea of representing uncertainty (which, in this case, is modelled with a stochastic process) using scenario trees. In this thesis, we developed a methodology that starts with available historical data; generates a set of scenarios for each random variable of the MSP model; defines individual scenarios that are used to build the initial stochastic process (as a fan or an initial scenario tree); and builds the final scenario trees that are the approximation of the stochastic process. |

| URL | Click Here |

| Export | Tagged XML BibTex |

New paper published in International Journal of Production Research.

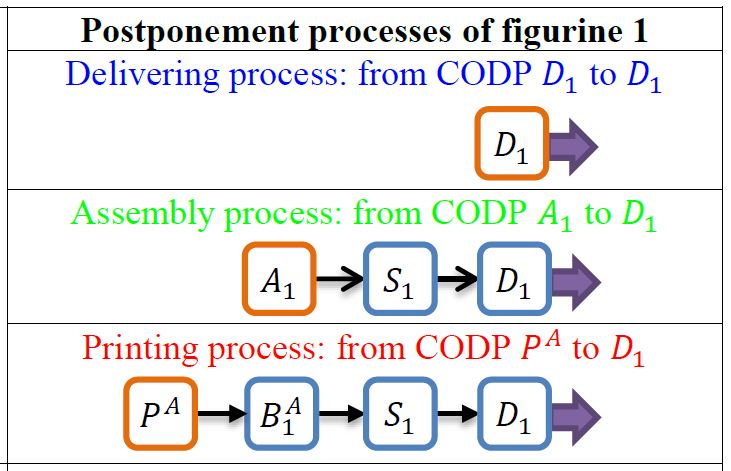

Tue, 07/21/2020 - 16:46 — admin The paper entitled Optimal Postponement in Supply Chain Network Design Under Uncertainty: An Application for Additive Manufacturing (preprint ) has been published in the International Journal of Production Research. This paper is the result of projects Strategical Models in Supply Chain Design, and Digitalizing Supply Chain Strategy with 3D Printing a successful collaboration between GNOM with Accenture Technology Labs (Silicon Valley), Accenture Analytics Innovation Center (Barcelona) and the Fundació CIM-UPC. This study This study presents a new two-stage stochastic programming decision model for assessing how to introduce some new manufacturing technology into any generic supply and distribution chain. It additionally determines the optimal degree of postponement, as represented by the so-called customer order decoupling point (CODP), while assuming uncertainty in demand for multiple products. Finally, it presents and analyses a case study for introducing additive manufacturing technologies.

The paper entitled Optimal Postponement in Supply Chain Network Design Under Uncertainty: An Application for Additive Manufacturing (preprint ) has been published in the International Journal of Production Research. This paper is the result of projects Strategical Models in Supply Chain Design, and Digitalizing Supply Chain Strategy with 3D Printing a successful collaboration between GNOM with Accenture Technology Labs (Silicon Valley), Accenture Analytics Innovation Center (Barcelona) and the Fundació CIM-UPC. This study This study presents a new two-stage stochastic programming decision model for assessing how to introduce some new manufacturing technology into any generic supply and distribution chain. It additionally determines the optimal degree of postponement, as represented by the so-called customer order decoupling point (CODP), while assuming uncertainty in demand for multiple products. Finally, it presents and analyses a case study for introducing additive manufacturing technologies.

Optimal Postponement in Supply Chain Network Design Under Uncertainty: An Application for Additive Manufacturing

Tue, 07/21/2020 - 15:49 — admin| Publication Type | Journal Article |

| Year of Publication | 2021 |

| Authors | Daniel Ramón-Lumbierres; F.-Javier Heredia; Joaquim Minguella-Canela; Asier Muguruza-Blanco |

| Journal Title | International Journal of Production Research |

| Pages | 5198-5215 |

| Journal Date | 07/2020 |

| Publisher | Taylor&Francis |

| ISSN Number | 0020-7543 |

| Key Words | manufacturing; postponement; stochastic programming; supply chain network design; 3D printing; additive manufacturing; research; paper |

| Abstract | This study presents a new two-stage stochastic programming decision model for assessing how to introduce some new manufacturing technology into any generic supply and distribution chain. It additionally determines the optimal degree of postponement, as represented by the so-called customer order decoupling point (CODP), while assuming uncertainty in demand for multiple products. To this end, we propose here the formulation of a generic supply chain through an oriented graph that represents all the deployable alternative technologies, which are defined through a set of operations that are characterized by lead times and cost parameters. Based on this graph, we develop a mixed integer two-stage stochastic program that finds the optimal manufacturing technology for meeting each market’s demand, each operation’s optimal production quantity, and each selected technology’s optimal CODP. We also present and analyse a case study for introducing additive manufacturing technologies. |

| URL | Click Here |

| DOI | 10.1080/00207543.2020.1775908 |

| Preprint | http://hdl.handle.net/2117/327874 |

| Export | Tagged XML BibTex |

A multistage stochastic programming model for the optimal bid of a wind producer

Wed, 07/11/2018 - 11:20 — admin| Publication Type | Conference Paper |

| Year of Publication | 2018 |

| Authors | F.-Javier Heredia; Marlyn D. Cuadrado; J.-Anton Sánchez |

| Conference Name | 23th International Symposium on Mathematical Programming |

| Conference Date | 01-06/07/2018 |

| Conference Location | Bordeaux |

| Type of Work | contributed presentation |

| Key Words | research; Battery energy storage systems; Electricity markets; Ancillary services market; Wind power generation; Virtual power plants; Stochastic programming |

| Abstract | Abstract: Battery Energy Storage Systems (BESS) can be used by wind producers to improve the operation of wind power plants (WPP) in electricity markets. Associating a wind power plant with a BESS (the so-called Virtual Power Plant (VPP)) provides utilities with a tool that converts uncertain wind power production into a dispatchable technology that can operate not only in spot and adjustment markets (day-ahead and intraday markets) but also in ancillary services markets that, up to now, were forbidden to non-dispatchable technologies. We present in this study a multi-stage stochastic programming model to find the optimal operation of a VPP in the day-ahead, intraday and secondary reserve markets while taking into account uncertainty in wind power generation and clearing prices (day-ahead, secondary reserve, intraday markets and system imbalances). A new forecasting procedure for the random variables involved in stochastic programming model has been developed. The forecasting model is based on Time Factor Series Analysis (TFSA) and gives suitable results while reducing the dimensionality of the forecasting mode. The quality of the scenario trees generated using the TFSA forecasting models with real electricity markets and wind production data has been analysed through multistage VSS. |

| URL | Click Here |

| Export | Tagged XML BibTex |

On optimal participation in the electricity markets of wind power plants with battery energy storage systems

Tue, 05/15/2018 - 16:25 — admin| Publication Type | Journal Article |

| Year of Publication | 2018 |

| Authors | F.-Javier Heredia; Marlyn D. Cuadrado; Cristina Corchero |

| Journal Title | Computers and Operations Research |

| Volume | 96 |

| Pages | 316-329 |

| Journal Date | 08/2018 |

| Publisher | Elsevier |

| ISSN Number | 0305-0548 |

| Key Words | research; Battery energy storage systems; Electricity markets; Ancillary services market; Wind power generation; Virtual power plants; Stochastic programming; paper |

| Abstract | The recent cost reduction and technological advances in medium- to large-scale battery energy storage systems (BESS) makes these devices a true alternative for wind producers operating in electricity markets. Associating a wind power farm with a BESS (the so-called virtual power plant (VPP)) provides utilities with a tool that converts uncertain wind power production into a dispatchable technology that can operate not only in spot and adjustment markets (day-ahead and intraday markets) but also in ancillary services markets that, up to now, were forbidden to non-dispatchable technologies. What is more, recent studies have shown capital cost investment in BESS can be recovered only by means of such a VPP participating in the ancillary services markets. We present in this study a multi-stage stochastic programming model to find the optimal operation of a VPP in the day-ahead, intraday and secondary reserve markets while taking into account uncertainty in wind power generation and clearing prices (day-ahead, secondary reserve, intraday markets and system imbalances). A case study with real data from the Iberian electricity market is presented. |

| URL | Click Here |

| DOI | 10.1016/j.cor.2018.03.004 |

| Preprint | http://hdl.handle.net/2117/118479 |

| Export | Tagged XML BibTex |